Samsung's Robotics Bet: Why Rainbow Robotics Matters to WPAI

Inside WisdomTree's Physical AI ETF — a closer look at Samsung's humanoid robotics subsidiary.

This is Part 3 of 4 in our deep look at the WisdomTree Physical AI, Humanoids and Drones UCITS ETF (ISIN: IE000LCKJ888). In Part 1, we covered the theme, the fund, and why it matters. In Part 2, we went inside Ubtech Robotics. Here, we look at Samsung’s robotics bet. Subscribe for free so you don’t miss the rest.

The Samsung Catalyst

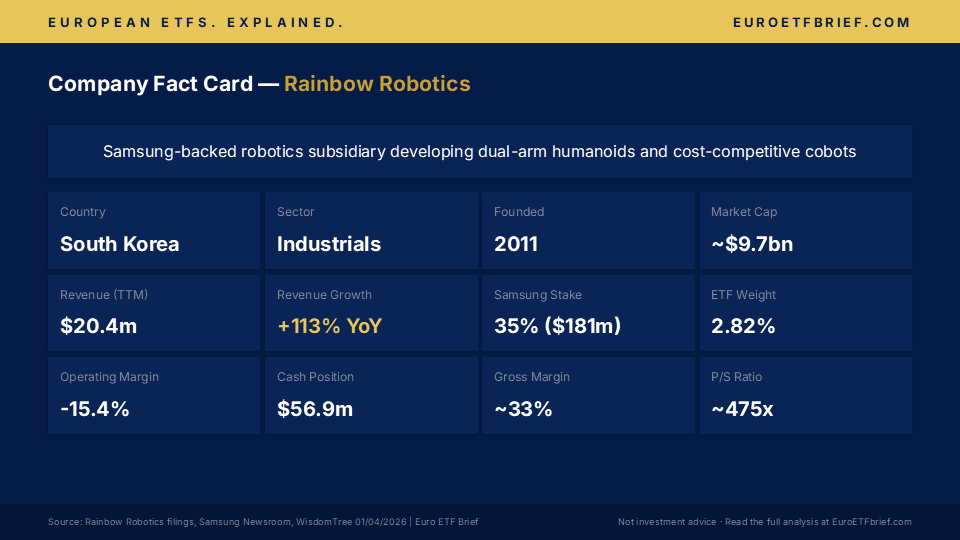

In March 2025, Samsung Electronics cemented its controlling stake in Rainbow Robotics, boosting its ownership to 35% for $181 million and establishing a dedicated Future Robotics Office reporting directly to Samsung’s CEO. The move signals Samsung’s conviction that humanoid robots and collaborative automation are not peripheral bets but central to the company’s next decade. For WPAI investors, Rainbow’s inclusion—at a 2.82% weight—reflects the fund’s thesis that the robotics race is being won not in Silicon Valley but by hardware-first incumbents in Asia.

What They Do

Rainbow Robotics designs and manufactures collaborative robots (cobots) and humanoid platforms. Founded in 2011 by roboticists from the Korea Advanced Institute of Science & Technology (KAIST), the company has built a distinctive supply chain: it manufactures most of its own actuators, encoders, and control systems in-house, allowing gross margins around 33% and pricing roughly 30% below Western competitors like Universal Robots and KUKA.

The product line spans three tiers:

RB Series cobots (5-16 kg payload): The RB5-850 costs €23,500 (~$25,500 USD) for a 5 kg payload and 927 mm reach; the RB10-1300 costs €33,000 (~$36,000 USD) with 10 kg payload and the longest reach in the lineup. Both achieve ±0.05 mm repeatability and support arc welding, CNC machine tending, and assembly.

RB-Y1 dual-arm manipulator: Unveiled in 2024 and now in production, this wheeled torso (131 kg, 140 cm tall, 24 degrees of freedom) targets research institutions and AI developers. Each arm handles 3 kg; the platform runs ~3 hours per charge at speeds up to 1.5 m/s. Leading universities including MIT, UC Berkeley, and Georgia Tech have pre-ordered units. The recent addition of Mecanum wheels (360-degree omnidirectional motion) and an open SDK expanded applicability.

Service robots and research platforms: Legacy products include the DRC-Hubo bipedal humanoid and Jay multimedia robot.

Revenue growth has been explosive: 30.75 billion KRW (~$20.4 million USD) in trailing twelve months, up 113% year-over-year, driven by RB Series ramp and RB-Y1 pre-orders. The company remains deeply unprofitable—operating margin was -15.4% in the most recent period—but sits on a fortress balance sheet: 85.6 billion KRW (~$56.9 million USD) in cash against negligible debt (228.9 million KRW).

At current valuation (market cap 14.57 trillion KRW, or ~$9.68 billion), Rainbow’s trailing price-to-sales ratio stands at nearly 475x — an extraordinary multiple that reflects investors’ belief in long-term upside rather than near-term earnings. For context, mature industrial automation firms trade at 25–50x earnings; even high-growth SaaS companies rarely exceed 20x sales.

Why It Matters for the ETF Theme

Rainbow Robotics embodies the “physical AI” thesis in two ways:

First, the product roadmap aligns with the next-generation factory concept. The RB-Y1’s dual-arm dexterity, wheeled mobility, and open SDK position it as a platform for AI-powered manipulation in dynamic environments—precisely what logistics hubs and smart factories need. Samsung’s willingness to fund RB-Y1 development as a subsidiary suggests the company sees this not as a niche research tool but as infrastructure for Samsung’s own automation ambitions. When Samsung Heavy Industries partnered with Rainbow in October 2025 to develop AI robots for shipbuilding, it validated the cross-group strategy.

Second, accessibility. The KOSDAQ is not readily accessible to European retail investors; trading occurs in Korean Won, with limited infrastructure for foreign settlement. The ETF—through full replication—brings exposure to a pure-play robotics developer that would otherwise require custodial workarounds. At 2.82% weight, Rainbow receives a proportional allocation according to the WisdomTree Physical AI Index methodology, which caps individual holdings and rebalances quarterly. This structure means your WPAI position automatically reflects Rainbow’s weighting adjustments without requiring active decisions.

The Samsung relationship carries both opportunity and risk. Integration into Samsung’s supply chain (particularly Samsung Heavy Industries and Samsung Electronics’ manufacturing divisions) provides de facto first-mover advantage in key end-markets. However, it also creates dependency risk, discussed below.

Risks & Considerations

Profitability and burn rate. Rainbow has never posted an operating profit, with margins at -15% in the latest period and free cash flow negative in all but one year of the past five years. Though cash reserves are robust, the company must either reach unit profitability or secure future funding. At such an extraordinary premium, any delay in margin expansion could precipitate a sharp revaluation.

Samsung dependency. While Samsung’s backing lends credibility and capital, it also concentrates customer and strategic risk. Samsung now controls 35% of voting shares and Rainbow is technically a subsidiary. If Samsung’s robotics roadmap pivots—or if geopolitical tensions limit Samsung’s ability to co-develop with Rainbow—the company loses leverage. Additionally, if Samsung eventually seeks full ownership and pays less than current market prices, minority shareholders face dilution risk.

Competitive intensity. Hyundai Motor Group owns Boston Dynamics (acquired 2020) and has partnered with Toyota on humanoid co-development. NVIDIA’s Jetson platform powers numerous competitor robots. While Rainbow’s cost structure is a genuine advantage, sustained success requires continuous AI integration and software ecosystem expansion. This is an area where larger tech incumbents have natural advantages.

Geopolitical and export exposure. South Korea sits at the nexus of U.S.-China tech competition. While robotics itself is not as tightly controlled as semiconductors, the RB-Y1’s advanced sensing, AI capability, and potential defense applications mean it could face export restrictions if U.S.-Korea export control frameworks expand. In August 2025, the U.S. rescinded “Validated End User” status for Samsung Electronics and SK Hynix, requiring individual licenses for semiconductor equipment imports to China. Robotics could face similar scrutiny, particularly if humanoid robots are deemed “dual-use” technology.

Valuation at a premium growth multiple. The current price-to-sales ratio assumes vast future market expansion and margin recovery. Execution risk is high. Even if the RB-Y1 succeeds in academia and logistics, commercialising humanoid robots at scale — and achieving the software-driven margins that would justify current pricing — remains unproven.

Conclusion

Rainbow Robotics represents a bet on two intertwined trends: that Samsung can build a world-class robotics division, and that dual-arm humanoids plus cost-efficient cobots will reshape manufacturing in the next five years. The company’s South Korean heritage, in-house supply chain, and Samsung backing are genuine strengths in a crowded field. WPAI’s 2.82% allocation captures this exposure with the discipline of quarterly rebalancing, insulating you from the need to time Rainbow’s execution. Yet the extraordinary valuation is a reminder that this is a growth play, not a value story — meaningful margin expansion and revenue scale are priced in.

This Series: Company by Company Through the ETF

Part 1: ETF Spotlight — When AI Learns to Walk

The full analysis of the WisdomTree Physical AI, Humanoids and Drones UCITS ETF — the theme, the index, the holdings, and the risks.

Part 2: Ubtech Robotics — From Prototype to Production

The ETF’s largest holding has shipped over 1,000 humanoid robots and signed partnerships from BYD to Airbus. We look at the numbers behind the Walker S2 and what a ~20x price-to-sales multiple is really paying for.

Part 4: Red Cat Holdings — The Rearmament Tailwind

From the U.S. Army’s Short Range Reconnaissance programme to NATO’s approved catalogue, this defence drone specialist is scaling fast on the back of a geopolitical shift.

Don’t miss the rest of the series. Subscribe to Euro ETF Brief — it’s free — and all parts will land in your inbox as they publish.

Sources

Samsung Newsroom: Samsung Becomes Largest Shareholder in Rainbow Robotics

The Robot Report: Samsung Establishes Future Robotics Office

Stock Analysis: Rainbow Robotics Market Cap & Revenue (KOSDAQ:277810)

Korea Tech Today: U.S. Export Controls Reshape South Korea’s Strategy

Disclaimer: This article does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The information contained herein is for educational and informational purposes only and does not replace individual advice from a qualified financial advisor. All investments carry risk, and the value of investments can fluctuate. Your capital is at risk, and past performance is not a reliable indicator of future results. While we strive to ensure the accuracy of the information provided, we make no representations or warranties regarding its completeness or accuracy. Disclosure: The author holds positions in the ETFs or securities mentioned.