Red Cat: The US Drone Play Riding NATO's Rearmament Wave

Inside WisdomTree's Physical AI ETF — a defence drone specialist riding the NATO spending wave.

This is Part 4 of 4 in our deep look at the WisdomTree Physical AI, Humanoids and Drones UCITS ETF (ISIN: IE000LCKJ888). In Part 1, we covered the theme, the fund, and why it matters. In Parts 2 and 3, we went inside Ubtech Robotics and Rainbow Robotics. Here, we look at the ETF’s defence drone play. Subscribe for free so you don’t miss future series.

The Rearmament Tailwind

In September 2025, Red Cat Holdings announced that its Black Widow system had been approved for the NATO Support and Procurement Agency (NSPA) catalogue — a milestone that lets all 32 NATO members and eligible partners procure the drone through standardised channels. Six months later, in March 2026, the company reported a 1,985% quarter-over-quarter revenue surge to $26.2 million for Q4 2025, driven largely by production ramp-up of the Black Widow for the U.S. Army. The company is no longer a speculative small-cap with a single customer; it’s now executing on real, tangible contracts at scale.

What They Do

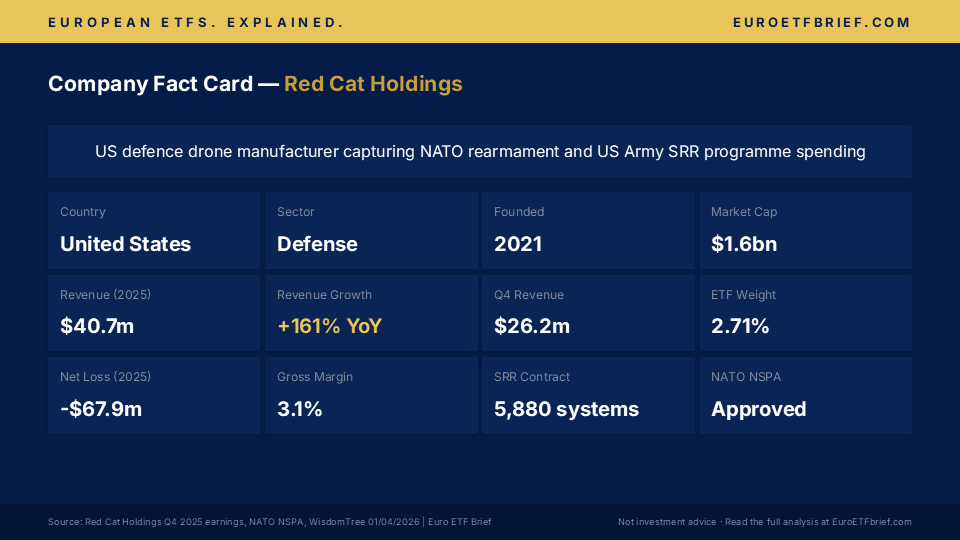

Red Cat Holdings designs and manufactures small unmanned aircraft systems (sUAS) and robotic solutions for defense, national security, and public safety. The company is built around three core subsidiaries: Teal Drones (sUAS and tactical systems), FlightWave Aerospace (long-endurance and VTOL platforms), and Blue Ops (uncrewed surface vessels).

The star product is the Black Widow, a tactical reconnaissance drone weighing under 3 pounds and featuring Teledyne FLIR’s Hadron 640R EO/IR thermal imaging and embedded AI. It delivers over 45 minutes of endurance, integrates secure long-range communications, and is designed to operate in electronic warfare (EW) environments. The company also produces the Teal 2 (military and public-safety short-range reconnaissance variant, starting around $15,000–$20,000 per unit with payloads), the FANG (first-person-view tactical drone), and the Edge 130 (a longer-endurance vertical takeoff and landing fixed-wing platform for extended-range intelligence, surveillance, and reconnaissance missions).

In 2025, Red Cat reported $40.7 million in full-year revenue, a 161% jump from $15.6 million in 2024. However, the company posted a net loss of $67.9 million, reflecting aggressive R&D, manufacturing build-out, and sales spending rather than cost discipline. At current market cap ($1.6 billion), the stock trades on roughly 39x sales — well above the aerospace and defence industry median of 5x and significantly ahead of AeroVironment, the closest publicly traded peer in the US tactical drone space, which trades at roughly 6x sales on $700 million in revenue. You’re paying a premium for growth and scale potential.

Why It Matters for the ETF Theme

This is the drone company that complements the ETF’s humanoid holdings. While humanoid robotics holdings like Ubtech and Rainbow Robotics capture long-term manufacturing automation, Red Cat addresses an immediate, tangible demand driver: NATO rearmament.

The Defence Spending Tailwind

Europe is in the midst of historic military rearmament. Germany’s 2026 defence budget is €108.2 billion (up sharply from €86 billion in 2025), and the Zeitenwende—the German government’s policy shift acknowledging a “wake-up call” on security—has embedded structural defense spending increases across Europe. NATO members are now committing to spend 3.5% of GDP on core defence by 2035, and 1.5% on defence-related projects. In 2025, all NATO Allies except Iceland met the 2% spending target for the first time. This isn’t cyclical; it’s structural.

Red Cat’s path to European customers runs through NATO’s standardized procurement channels. The Black Widow’s inclusion in the NSPA catalogue means allied procurement officers can order directly without lengthy bilateral negotiations. Red Cat has already secured orders from one Asia-Pacific NATO ally (partner nations in the Indo-Pacific region), signaling international traction.

Contract Wins & Scale

In 2024, Red Cat was selected as the production winner for the U.S. Army’s Short Range Reconnaissance (SRR) Program of Record — a total of 5,880 systems (each consisting of two aircraft). This replaced Skydio on the contract and delivered immediate revenue visibility. The company expanded total manufacturing footprint by 520% to 254,000 square feet by year-end 2025, physically demonstrating intent to scale.

Index Mechanics: Why 2.71%?

Unlike traditional market-cap-weighted indices, the WisdomTree Physical AI Index starts from an equal-weight base and then adjusts each holding by two proprietary scores: a Thematic Score (reflecting the importance of the company’s category to the overall Physical AI theme) and a Relevancy Score (measuring how closely the company’s core business is tied to that theme). Red Cat’s 2.71% weight reflects its high relevancy as a pure-play defence drone manufacturer — its entire business is unmanned systems, which scores well against diversified conglomerates where drones are a side project. Quarterly rebalancing and capping rules apply, so if Red Cat’s stock rallies sharply, its weight may be trimmed to maintain diversification across the portfolio’s roughly 61 holdings.

Risks & Considerations

Red Cat trades on a premium growth multiple, meaning you’re betting on sustained revenue expansion and eventual profitability. Several headwinds could derail that narrative.

Path to Profitability Unclear

Despite 161% revenue growth, the company reported a $67.9 million loss in 2025 and is forecast to remain unprofitable through at least 2028. Gross margins stand at a wafer-thin 3.1%, and management has declined to provide a profitability timeline. This is typical for defense contractors in heavy investment phases, but it means negative cash burn will persist unless revenue accelerates further.

Customer and Contract Concentration

A significant portion of Red Cat’s $40.7 million 2025 revenue came from the U.S. Army SRR contract ramp-up. If the Army slows procurement, reduces order volumes, or extends delivery timelines, Red Cat’s growth rate could decelerate sharply. European NATO members have approved Black Widow through NSPA, but actual order flow remains unproven at scale.

Manufacturing Execution Risk

Red Cat has tripled manufacturing footprint in one year. Scaling production while maintaining quality control, managing supply chains, and training personnel are real operational challenges. Any manufacturing delays or quality issues could strain customer relationships and defense contract compliance.

Geopolitical Sensitivity

Red Cat benefits from elevated global tensions and NATO rearmament. However, a significant de-escalation in Ukraine, a shift in US defense policy, or budget pressures in Europe could curtail orders. Defense budgets are politically volatile.

Export Controls and ITAR

Red Cat’s drones are subject to the International Traffic in Arms Regulations (ITAR), which restrict export of US-origin defense articles to foreign countries without State Department license approval. This limits international expansion to NATO allies and approved partners only. A shift in US export policy could either open or constrain markets. Additionally, the company must maintain strict cybersecurity and supply chain integrity standards to retain Blue UAS (approved vendor list for US military drones) certification—any lapses could jeopardize clearance.

Conclusion

Red Cat Holdings is a well-positioned bet on NATO rearmament and US defense spending, with real contracts and proven production ramp. The Black Widow’s NATO NSPA approval and strong Q4 2025 results are tangible catalysts. However, the premium valuation leaves little room for execution missteps, and the path to profitability remains foggy. For the WPAI ETF, Red Cat provides concentrated exposure to tactical unmanned systems—a hardware play distinct from the humanoid robotics theme—and geographic diversification beyond Asian small-cap risk. Worth watching, but not without risk.

This Series: Company by Company Through the ETF

Part 1: ETF Spotlight — When AI Learns to Walk

The full analysis of the WisdomTree Physical AI, Humanoids and Drones UCITS ETF — the theme, the index, the holdings, and the risks.

Part 2: Ubtech Robotics — From Prototype to Production

The ETF’s largest holding has shipped over 1,000 humanoid robots and signed partnerships from BYD to Airbus. We look at the numbers behind the Walker S2 and what a ~20x price-to-sales multiple is really paying for.

Part 3: Rainbow Robotics — The Samsung Catalyst

Samsung invested $181 million for a 35% controlling stake and built a dedicated robotics office around this Korean cobot maker. At nearly 475x trailing sales, the market is pricing in a future that hasn’t arrived yet.

Enjoyed this series? Subscribe to Euro ETF Brief — it’s free — and you’ll be the first to read our next deep look at a European thematic ETF.

Sources

Red Cat Holdings: U.S. Army SRR Programme Selection (Investor Relations)

Red Cat: Record Q4 Revenue Growth, 161% Full-Year Increase (Investor Relations)

Black Widow Approved for NATO NSPA Catalogue (Investor Relations)

Teledyne FLIR Selected as Thermal Camera Provider for SRR Programme

Germany’s Path to Kriegstüchtigkeit: The 2026 Defence Budget (Atlas Institute)

Disclaimer: This article does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The information contained herein is for educational and informational purposes only and does not replace individual advice from a qualified financial advisor. All investments carry risk, and the value of investments can fluctuate. Your capital is at risk, and past performance is not a reliable indicator of future results. While we strive to ensure the accuracy of the information provided, we make no representations or warranties regarding its completeness or accuracy. Disclosure: The author holds positions in the ETFs or securities mentioned.